Equity Research Notes: McDonald's (MCD) - January 12, 2026

McDonald's (MCD) – Personal DCF Valuation Note – January 12, 2026 Mildly Bullish: Quality Compounder with Modest Upside on Margin Leverage

(Disclaimer: This is my personal opinion and modeling exercise only, not financial, investment, or professional advice. I am not a CFA, registered analyst, or advisor. All views are mine, based on public data. Investing involves substantial risk of loss. Do your own research and consult qualified professionals. Past performance has no guarantee of future results. Full disclaimer at end.)

Data & Timing Note

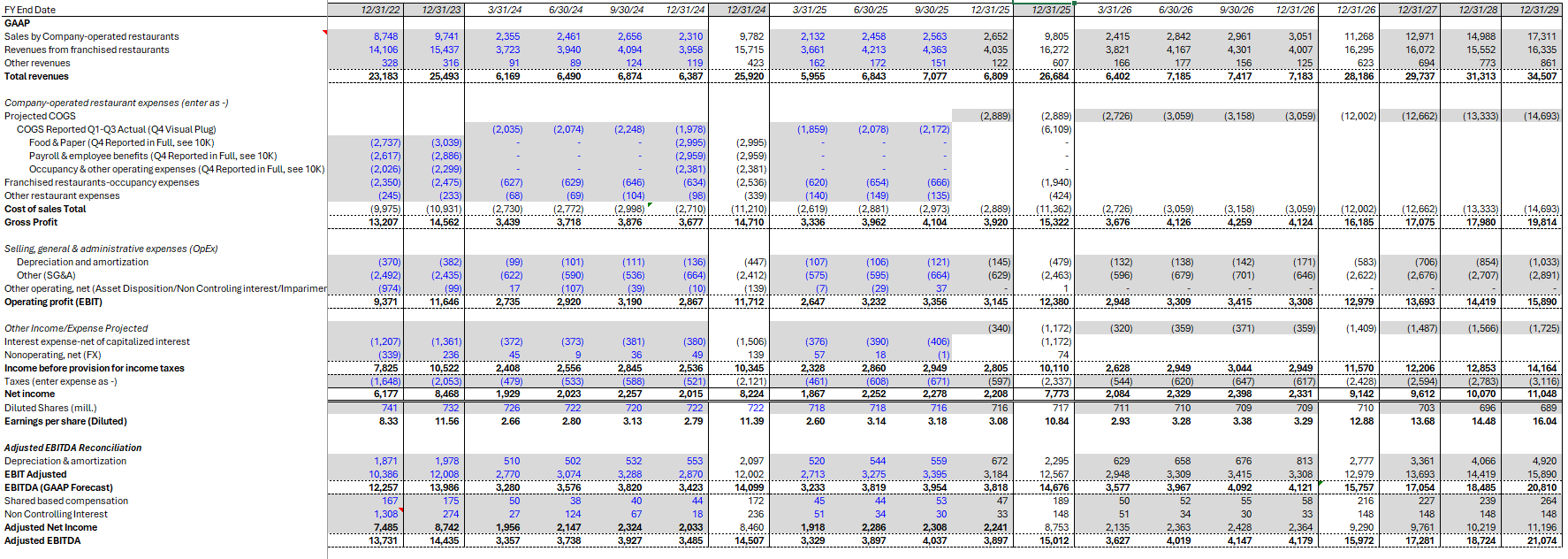

MCD Q4/FY2025 results are not yet released (expected early-February). 2024 - 2025Q3 figures are reported actuals; 2025Q4 onwards uses estimates (Q4 projected); Forecasts beyond are my projections, actuals may vary.

Executive Summary

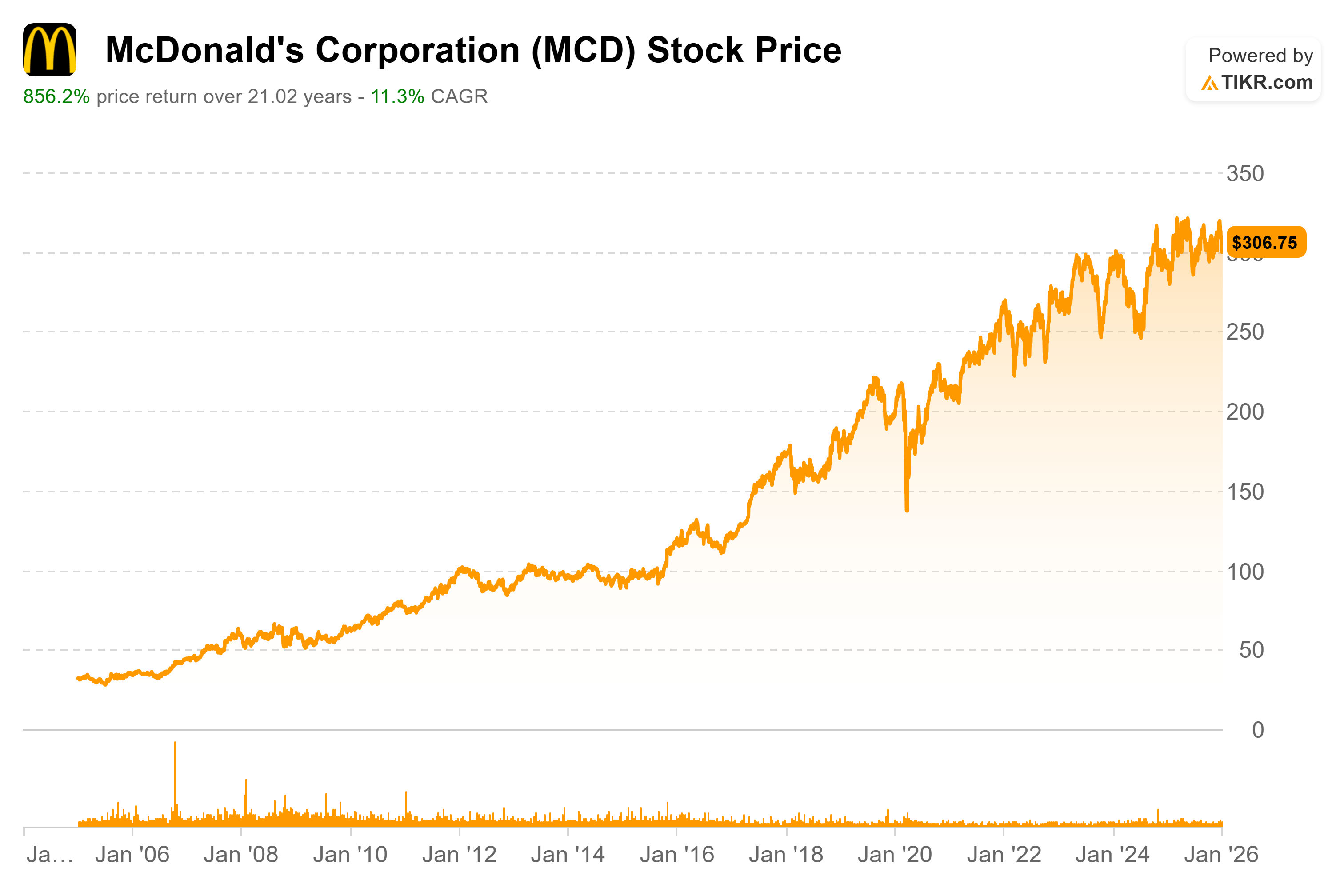

· Current Price (Jan 12, 2026): ~$307

· My DCF-Derived Fair Value: $330.90 (Price as of Jan 12, 2026, DCF valuation set to Dec 31, 2025, FY25 Results Expected February 9, 2026)

· DCF-implied upside: ~ 8% to $330.90 target price, plus ~ 2.4% dividend yield (total expected return ~ 10.2%)

· Personal View: Overweight on dips, defensive staple with compounding power.

Investment Thesis - McDonald’s is a world class, asset light franchise model (~ 95% franchised)[1] with durable pricing power, strong digital/reward tailwinds, and consistent FCF generation. Near-term consumer caution (value focus, macro sociological and economic pressures) limits explosive growth, but my forecasts show solid mid-single-digit revenue and meaningful EBITDA margin expansion (to ~14.3% by 2029) efficiency, menu enhancements, and global scale. At current levels (~17.44x Forward EV/EBITDA),[2] the stock is fairly valued, but my assumptions justify a modest upside (implied NTM EV/EBITDA 18.2x) with ~ 8% upside with an additional ~ 2.4% dividend yield.

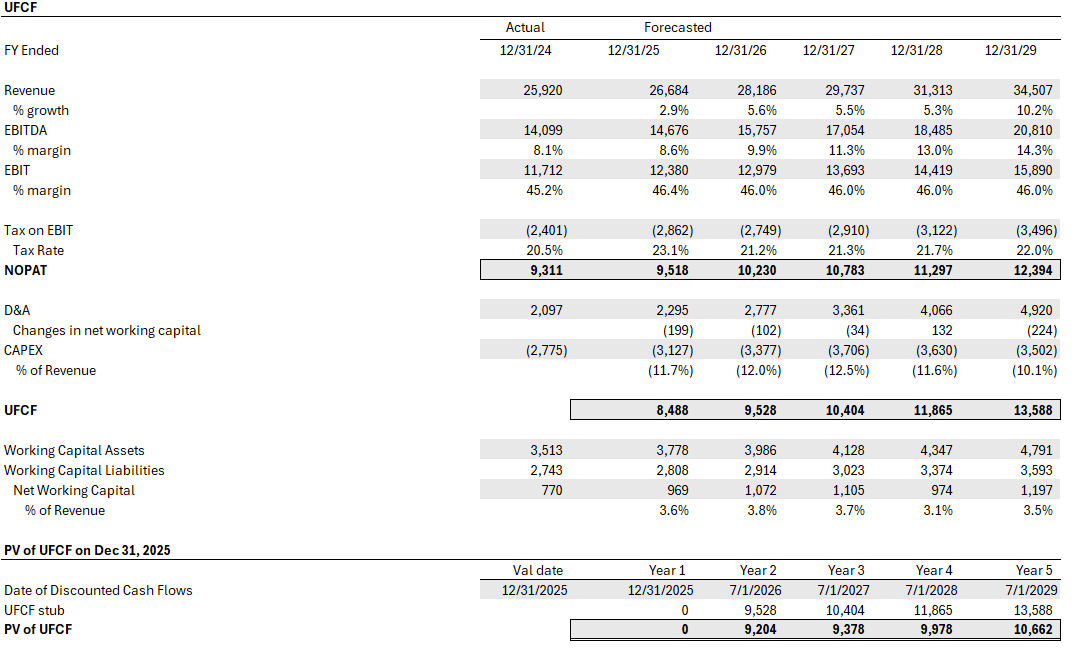

Valuation Summary I constructed a 2-stage unlevered DCF (UFCF-based) with mid-year discounting:

Explicit period: 2025–2029 (revenue growth 2.9–10.2%, EBITDA margins ramping to 14.3%, capex ~10–12.5% of revenue).

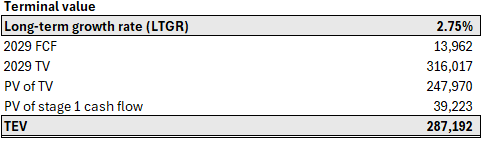

Terminal: 2.75% LTGR.

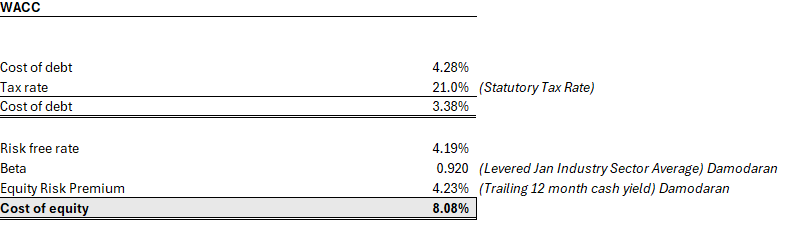

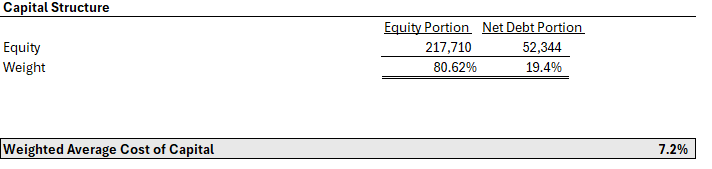

WACC: ~7.2% (Rf 4.19%, beta 0.92 from Damodaran industry avg, ERP 4.23% trailing cash yield, tax 21% statutory marginal).[3]

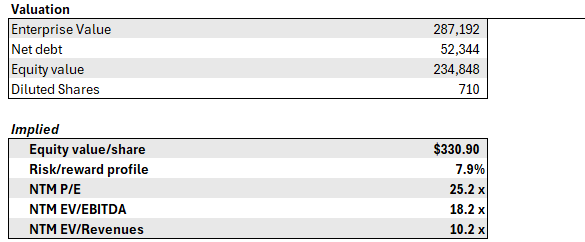

TEV: $287.2B → Equity Value/Share: $330.90 (after $52.3B net debt, 710M diluted shares).

Key Implied Multiples from Model

NTM P/E: 25.2x

NTM EV/EBITDA: 18.2x

NTM EV/Revenues: 10.2x

These reflect a modest premium to current market forwards (e.g., implied NTM P/E 25.2x vs. GuruFocus consensus forward P/E 23.17x)

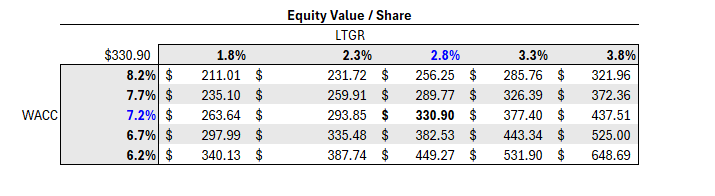

Sensitivity Analysis

Financial & Operational Highlights

Earning drivers: Pricing power, digital/reward loyalty, marginal international markets expansion.

Margin expansion: EBITDA to 14.3% by 2029

FCF profile: Strong conversion, supporting dividends (~2.4% yield) and buybacks.

Balance sheet: Asset-light business model with strong investment-grade credit profile.

Market & Consensus Context

Consensus analyst target: 23 analysts rated at “Moderate Buy” ~$305–375 (Average Price Target $338.89).[4]

Market multiples: Trailing P/E Ratio 26.17, Forward P/E 23.17, Trailing EV/EBITDA ~18.9x, EV/ Forward EBITDA ~17.44, EV/Revenue ~10.35x trailing, EV/Forward Revenue ~9.6–10x.[5]

My model illustrated a more optimistic scenario, hence the modest premium.

Catalysts & Risks Upside Catalysts

A Stronger Consumer

Seen through expected digital reward/deal contribution and menu enhancements.

Continued franchise efficiency and emerging market expansion.

Fueled by the enduring aspirational draw of American fast-food culture.

Positive AI adoption and integration.

Sustained buybacks/dividends.

Recent dividend boost[6]

Downside Risks

Prolonged consumer weakness

Value wars, inflation/labor costs.

Higher than expected unemployment.

Negative feedback/integration via AI adoption.

Competitive pressure in quick service

From the shift toward health-conscious and wellness-oriented menu offerings.

Bottom Line McDonald’s is a high-quality compounder trading at fair value with modest upside under my base case. The franchise model and cash flow resilience provide a strong defensive edge. I see ~ 8% capital appreciation potential plus ~2.4% yield for total returns in the low-teens overtime.

Supplemental Data:

Important Disclaimer: The content on this blog, including this post, is for informational and entertainment purposes only. It does not constitute financial, investment, legal, or tax advice. I am not a registered investment advisor, broker, or financial professional.

Any opinions expressed are my own and based on publicly available information. They should not be relied upon for making investment decisions. Investing in stocks or any securities involves substantial risk of loss, and you could lose some or all of your money.

Always conduct your own due diligence and consult with qualified professionals before making any financial decisions. I make no guarantees about the accuracy or completeness of the information here.

[1] [2025 Q3 Earnings Release]

[2] [EV/EBITDA MCD ]